Home : FAQ

FAQ

| 1. | How to Open a NSDL demat account? |

| Answer |

Opening a demat account is quite simple. All you have to do is to approach a NSDL DP, which will help you to complete the formalities. You need to fill up a form, submit PAN card and proof of address. In addition, you need to provide details of your bank account. Alternatively, you can click on https://nsdl.co.in/Open_NSDL_Demat_Account.php to open your demat account. After your demat account is opened, your DP will provide you DP ID and Client ID, a copy of your Client Master Report containing your demat account related details, tariff sheet and ‘Rights & Obligations of Beneficial Owner and Depository Participant’. DP ID is 8 characters long code, (example IN3XXXXX) allotted by NSDL to all DPs to identify them. Client ID is 8 digit long code used to identify the clients in the system. Combination of DP ID and Client ID makes your unique account number in the NSDL system. You should verify the Client Master Report to ensure that all your details have been recorded correctly in depository system. If you want to trade in shares etc. (i.e. buy or sell), you would also need to open a Trading / Broking account with any SEBI registered stockbroker. There are many DPs which offer 3-in-1 arrangement for the benefit of investors (3-in-1 is a combination of demat account, trading account and bank account). Now a days many NSDL DPs enable their clients to open demat account online, thus making the process paperless and extremely convenient. |

| 2. | How do I select a DP? |

| Answer |

You can select your DP to open a demat account just like you select a bank for opening a savings account. Some of the important factors for selection of a DP can be:

For list of DP locations, visit https://nsdl.co.in/dpsch.php and for their comparative charge structure, visit https://nsdl.co.in/about/charges.php |

| 3. | Whether all the DPs are same? |

| Answer |

NSDL has specified certain basic eligibility criteria for becoming a DP. The criteria are similar or even higher in certain respects than the corresponding provisions of SEBI regulations. All the DPs are same in the sense they are appointed by NSDL only after grant of Certificate of Registration by SEBI to them. However, the type of services offered, service standards and charges for the services rendered may differ among DPs. |

| 4. | What should I do if I want to open a demat account? |

| Answer |

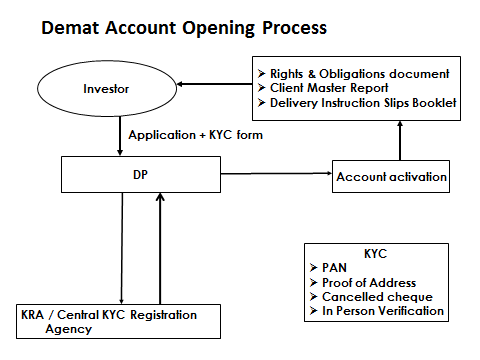

Once you have decided to open an account with a particular DP, you may approach that DP and fill up an account opening form. You would be required to provide your photograph and self-attested copy of following documents -

Please remember to take original documents to the DP for verification. In case you are unable to produce original document for verification, then photocopy should be attested by any authorized entity, like a public notary. Your DP may ask additional proof of identity / address to meet its requirements in addition to above-mentioned. The process of account opening is shown in the diagram below -

|

| 5. | What is in-person verification? |

| Answer |

It is mandatory to establish the identity of the applicant at the time of opening account as per SEBI guidelines. This is done by the DP’s staff by verifying the affixed photograph on account opening form and the photo seen on document on PAN card with the person seeking to open the account. For Joint account holders, the ’in-person verification’ is required for all the holders. |

| 6. | Can I open more than one demat account? |

| Answer |

Yes. You can open more than one account with the same DP. There is no restriction on the number of accounts you can open with a DP. |

| 7. | Do I have to keep any minimum balance of securities in my demat account? |

| Answer |

No. The depository has not prescribed any minimum balance. You can have zero balance in your demat account. |

| 8. | Why should I give my bank account details at the time of account opening? |

| Answer |

Providing bank account details at the time of demat account opening is mandatory. These bank details are communicated to issuer companies / RTAs for the purpose of crediting any amount payable to you (such as dividend, interest or maturity payment or redemption amount) directly in your bank account. It is therefore suggested that you provide details of your active bank account in the account opening form. Later, in case of change therein, please remember to inform to your DP. |

| 9. | What is 'Standing Instruction' given in the account opening form? |

| Answer |

In demat account, debit or credit transactions are permitted only if it is duly authorized by the respective holder(s). As a Delivery Instruction Slip (DIS) is required for every debit transfer in the demat account, a 'Receipt Instruction Slip' is required for every credit transfer in the demat account. By giving a onetime standing instruction to your DP, you may avoid giving receipt instruction to your DP whenever a credit is expected in the account. |

| 10. | Can I operate a joint account on "either or survivor" basis just like a bank account? |

| Answer |

No. As per rules applicable at present, demat account cannot be operated on 'either or survivor' basis like the bank account. Therefore, every instruction given for a jointly held demat account needs to be signed by all the joint holders. |

| 11. | Can I transfer all my securities to my account with another DP and close my demat account with one DP? |

| Answer |

Yes. In case you have multiple demat accounts with one or more DPs and do not wish to continue with them, you may submit account closure form to your DP(s) in prescribed format. In the form, you are required to mention DP ID, DP name and Client ID of the account where you wish the balances to be transferred. Your DP will transfer all your securities as per your instruction and close your demat account. It is important to understand that a demat account cannot be closed if there is any balance in the account. |

| 12. | What can I do with my NSDL demat account? |

| Answer |

There are numerous uses of your NSDL demat account. Few important things that you can do with your NSDL demat account are listed below – You may apply for IPOs and NFOs. Do not forget to mention your DP ID and Client ID correctly in the application form. Same demat account can be used to purchase and hold shares and other types of securities. You will automatically receive all corporate benefits (bonus, rights issue, etc.) in your demat account. Cash benefits like dividend declared by your company, interest or maturity amount payable on your bond investments etc. would be credited to bank account linked with your demat account. Please ensure correct bank account details are recorded in your demat account. You may use your demat account to avail 'loan against shares' facility which is offered by many banks etc. to meet your financial requirements without requiring to sell the investments. You may convert all your investments in shares, bonds, debentures, government securities, sovereign gold bonds etc. held in paper form to demat form through your DP. You may hold your mutual fund investments in the same demat account. Holding mutual fund units in demat account makes things a lot easier for you. You would be able to monitor your portfolio at one place through NSDL CAS. It also saves you from the need to engage with various mutual fund houses if you want to make any change in your personal information, for example, address or bank details or nominee, etc. You may subscribe to mutual fund units in demat form by simply mentioning your DP ID and Client ID in application form. Investment in mutual funds by way of SIP is also possible through your demat account. For redemption or repurchase of mutual fund units, you may give an instruction to your DP or may use NSDL's SPEED-e facility. You may participate in buyback offer by tendering your shares to company through your demat account. You may participate in securities lending and borrowing scheme by lending securities lying idle in your demat account and may earn market returns. |

| 13. | How can I shift or transfer my demat account from one DP to another DP? |

| Answer |

For shifting or transfer of a demat account, you need to first open a new demat account where you want the balances to be transferred to (if you already have another demat account, then you may use it for this purpose, instead of opening a new account). Then you need to submit duly filled and signed ‘Account Closure Form’ to your existing DP. In the form, you should mention the details of the other demat account where you want the balances to be transferred. After verification of your request, your DP will arrange to transfer the balances to the desired account and then close the source account. |

| 1. | What is dematerialization? |

| Answer |

Dematerialization is the process by which physical certificates of securities are converted into securities in electronic form by way of credit in investor's demat account held with a DP. Dematerialization is change in form of holding, it does not result into change of ownership. |

| 2. | How can I dematerialize my securities certificates? |

| Answer |

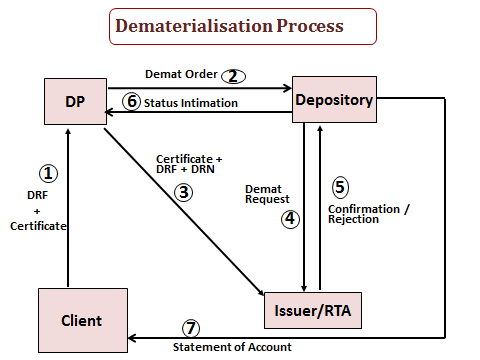

In order to dematerialize certificates, you need to open a demat account. Once the demat account has been opened, you need to fill up a 'Dematerialization Request Form' in prescribed form and submit it to your DP along with the security certificates. Your DP will forward the demat request to the concerned issuer company or its Registrar and Transfer Agent for further processing. Once the request is confirmed by the concerned issuer company or its Registrar and Transfer Agent, it results in credit of electronic securities in the demat account of the respective investor. The process of dematerialization is shown in the diagram below –

|

| 3. | Can I dematerialize any share certificate? |

| Answer |

No, not all the share certificates can be dematerialized. For dematerialization, following conditions should be met with -

Most of listed and active companies have already joined NSDL and their shares and other types of securities are available for demat. Many other companies are in the process of joining NSDL. You may search if the shares held by you are available for demat or not, at https://nsdl.co.in/master_search.php. |

| 3. | What precautions should I take before submitting my certificates to DP for dematerialization? |

| Answer |

You should take care of following -

After above steps, you may mark the share certificates that you wish to dematerialize with words 'Surrendered for Dematerialisation'. Your DP will provide you the rubber stamp to be used for this purpose. |

| 4. | How long does the dematerialization process take? |

| Answer |

As per SEBI's guidelines, DP is required to process the demat request received by it within 7 days. Further, issuer company / its RTA may take up to 15 days to process the demat request received by them. Considering the time required for transmission of documents from DP to issuer company / RTA, dematerialization will normally take about 30 days. |

| 5. | Can I open a single account to dematerialize securities owned individually and securities owned jointly along-with my wife? |

| Answer |

No. The demat account must be opened in the same ownership pattern in which the securities are held in the physical form. For example, if one share certificate is in your name and another certificate has your name along with your wife's name, then you would need to open two demat accounts (one in your name and other in joint names of yourself and your wife). |

| 6. | Do I have to dematerialize securities that I do not intend to sell? |

| Answer |

The Depositories Act, 1996 gives investors an option to hold securities in physical form or demat form. Hence, if you do not intend to sell the securities, you may not dematerialize them. However, holding the securities in demat form entails numerous benefits and is therefore highly recommended. Further, there are existing / proposed restrictions on transfer of securities belonging to listed companies and unlisted public limited companies, if held in physical form. It may therefore be better to dematerialize the securities. |

| 7. | Can I dematerialize my investment in tax-free bonds which are under lock-in? |

| Answer |

Yes. You can dematerialize your tax-free bonds even when they are under lock-in. The process of demat is similar to that applicable to demat of shares. You need to submit duly filled in and signed DRF to your DP along with bond certificates. DP will forward the request to concerned issuer / its RTA and upon confirmation, credit will be received in your demat account. |

| 8. | Can I purchase government securities directly in demat form? |

| Answer |

Yes. Now the market of government securities like bonds and Treasury Bills (T-Bills) is easily accessible to retail investors. In fact, RBI does keep a portion of new issues reserved for retail investors. You may invest in G-Sec by participating in auction of new securities or by purchasing already issued securities in secondary market. For both, you need to approach any authorized bank or primary dealer or stock broker, mentioning your demat accounts details (DP ID and Client ID). |

| 9. | How can I subscribe to Sovereign Gold Bonds (SGB) in demat form? |

| Answer |

The SGB offers a superior alternative to holding gold in physical form. Option to hold SGB in demat form makes it even better and convenient. The process to buy or subscribe to sovereign gold bonds in demat form is quite easy. All you need to do is to mention your DP ID and Client ID in your subscription form. Some banks offer online application facility also (if investor makes application online and does payment electronically, then some price discount is also available at present). Upon allotment by RBI, your demat account will credited with the requisite number of bonds. |

| 10 | Can I convert my investment in Sovereign Gold Bonds (SGB) held in paper form (Certificate of Holding form) into demat form? |

| Answer |

Yes, you may do so. For this purpose, you need to contact the bank / agent from whom you had purchased the SGBs. They will assist you in conversion of SGBs held in form of Certificate of Holdings into demat form. |

| 11. | Can I convert my investment in government securities held in SGL form to my demat account kept with NSDL DP? |

| Answer | Yes. You need to provide a duly filled in and signed request in prescribed format (known as Dematerialization Request Form - Government Securities) along with 'Form of Transfer' to your DP. Your DP will forward the request to NSDL. NSDL will arrange for necessary credit in your demat account. |

| 12. | I have physical certificates with the same combination of names, but the sequence of names is different. In some certificates, I am the first holder and my wife is the second holder, whereas in some other certificates, my wife is the first holder and I am the second holder. Do I need to open two different accounts for the purpose of dematerialization of these certificates? |

| Answer |

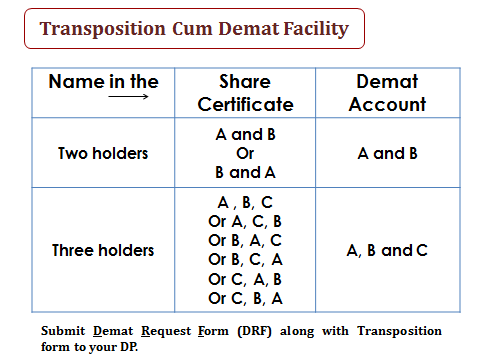

The joint holders are entitled to change the sequence of names by making a written request to the company. This does not constitute a transfer. Changing the sequence of joint holders is called 'Transposition'. However, transposition facility can be availed for entire holdings in a folio and not allowed for part of the holdings. If the same set of joint holders hold securities in different sequence of names, then there is no need to open multiple demat accounts for dematerialization of such securities. Using 'Transposition cum Demat facility' such securities held vide certificates in different combinations, can be dematerialized in one demat account. For this purpose, Dematerialization Request Form (DRF) and an additional form called 'Transposition cum Demat Form' should be submitted to the DP. This is explained in the diagram below -

|

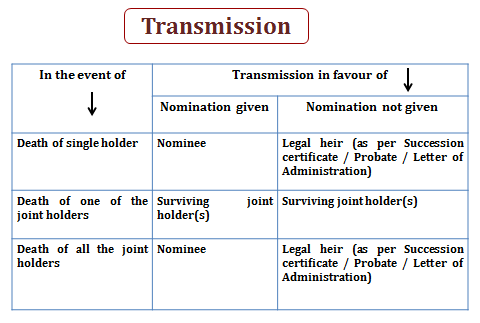

| 1. | What does transmission mean in relation to demat accounts? |

| Answer |

Transmission is the process of law by which securities belonging to a deceased account holder are transferred to surviving joint holder(s) / legal heirs / nominee of the deceased account holder. Process of transmission in case of dematerialized holdings is relatively convenient as the transmission formalities for all securities held in a demat account can be completed by submitting the requisite documents to DP. There is no need to approach various companies for this purpose, as is required when securities are held in physical form.

|

| 2. | What is the procedure for transmission of securities to the nominee in case of the death of the sole account holder? |

| Answer |

In case of the death of the sole holder, for transmission of securities, the nominee needs to submit duly filled-in transmission form along with a copy of the death certificate duly attested by a Notary Public or a Gazetted Officer. In case the account of the claimant is not with the same Participant, copy of Client Master Report of the account of the claimant (certified by the concerned DP) is also required. After verification of these documents, the DP will transmit the securities to the demat account of the nominee. |

| 3. | What would happen if there is no nominee in the demat account held by sole holder? |

| Answer |

In such a case, the securities would be transmitted to the account of legal heir(s), as may be determined by an order of the competent court. Following documents are required for this purpose -

However, if the value of securities to be transmitted is below ₹5,00,000/- (on the day of application for transmission), the DP may process the request based on following documents:

|

| 4. | What is the procedure for transmission in case of death of one or more joint holder(s)? |

| Answer |

In such a case, the securities would be transmitted to the surviving holder(s), irrespective of the nomination. For example, if the account is in the joint names of Mr. A, Mr. B and Mrs. C, in the event of the death of Mr. B, the securities will be transmitted to surviving holders that is, Mr. A and Mrs. C. The surviving holder(s) would need to submit the following documents to the DP:

|

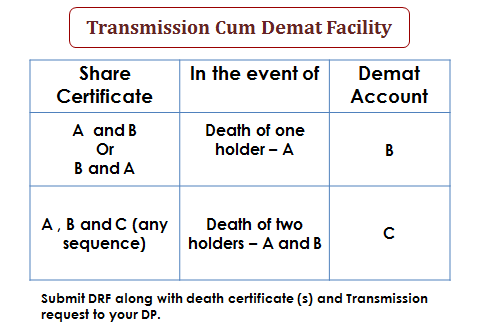

| 5. | What is the meaning of 'Transmission cum Demat'? |

| Answer |

'Transmission cum Demat' is a very useful facility when one of the joint holders mentioned in securities certificate (held in physical form) has died and remaining holder(s) wish to have the securities transmitted in their name in demat form. Using this facility the twin objectives of deletion of name of one of the deceased joint holders and dematerialization of securities can be achieved in a single step. This is explained in the diagram

|

| 1. | What is SMS Alert facility? |

| Answer | NSDL helps demat account holders to monitor the important transactions happening in their account by sending SMS alerts on their mobile number registered in the demat account. As the alerts are sent by NSDL directly, they reflect the true status of the demat account. This facility is completely Free for demat account holders. |

| 2. | How do I register for SMS Alert facility? |

| Answer |

In case you have not been using this facility already, you may register yourself simply by submitting a written request to your DP mentioning your mobile number. You will start receiving the alerts once your mobile number is successfully recorded and SMS flag for receiving SMS alerts option is enabled in depository system by your DP.

|

| 3. | For which transactions SMS Alerts are sent? |

| Answer |

a. All debit transfers For change of address, registration and de-registration of Power of Attorney in depository system, SMS alerts are sent to registered mobile phone irrespective of whether account holder has opted for this facility or not. |

| 4. | Why should I register for SMS Alert facility? |

| Answer |

NSDL directly sends messages for many important transactions carried out in demat account to the registered mobile number. This acts as an effective monitoring method to safeguard your demat account. |

| 5. | What are the charges for availing this facility? |

| Answer | No charge is levied by NSDL on DPs for providing this facility to account holder. |

| 6. | I have provided my mobile number to DP at the time of opening demat account. Do I still need to register for this facility? |

| Answer |

If you are not getting SMS alerts, you need to give a request to your DP to enable the SMS Alert flag in the depository system. Merely giving mobile number is not sufficient. |

| 7. | What should I do if I change my mobile number? |

| Answer |

In case you change your mobile number, you just need to provide your new mobile number to your DP in writing. Once change is effected by DP in depository system, you will receive a message on your old as well as new mobile number in this regard. In case you are considering changing your mobile number, you may like to opt for mobile number portability by which you may change your service provider but retain the current mobile number. |

| 8. | Is it mandatory for me to register for SMS Alert facility? |

| Answer |

No, except for individual accountholders who are having a Basic Service Demat Account and whose accounts are operated through Power of Attorney, this facility is not mandatory, but highly recommended. As the alerts are directly sent by depository, you are in position to monitor the important transactions happening in the account and take appropriate actions, if required. |

| 9. | What are the terms and conditions related to SMS Alert Service? |

| Answer |

The terms and conditions related to SMS Alert Services are available at https://nsdl.co.in/termsandconditions.php |

| 1. | What is the meaning of conversion of mutual fund units (represented by Statement of Account) into demat form? |

| Answer | If you are holding mutual fund units in physical form, which are represented by Statement of Account (SOA) and you want to hold them in demat form, you may do so by submitting a request in prescribed form to your DP. This is known as conversion of mutual fund units in demat form. |

| 2. | In case I do not have a demat account, what should I do? |

| Answer | In case you do not have a demat account and wish to convert your mutual fund investments in demat form, you need to open a demat account with any NSDL DP. |

| 3. | What are the advantages of holding mutual fund units in demat form? |

| Answer |

a. You receive a single consolidated account statement, which mentions all your investments in various securities including mutual fund units. You need not look at different statement received from mutual funds companies. |

| 4. | What is the procedure for converting mutual fund units (represented by Statement of Account) into demat form? |

| Answer | You need to submit a duly filled in Conversion Request Form (CRF) to your DP along with the Statement of Account. After necessary checks, your DP will forward your request to concerned AMC / its Registrar. Upon confirmation from AMC / Registrar, mutual fund units will be credited in your demat account. |

| 5. | Can Non Resident Indians (NRIs) convert the mutual fund units held under NRI status into demat form? |

| Answer | Yes, provided demat account is opened under NRI status. |

| 6. | How can I subscribe for mutual fund units through stock exchange platform? |

| Answer | You need to simply give a subscription order to your stockbroker along with the required amount. Your broker will enter the request on the platform of stock exchange. Upon receipt of units from AMC / Registrar on the payout day, your broker / clearing corporation will arrange to credit of desired mutual fund units in your demat account. |

| 7. | How do I redeem the mutual fund units held in my demat account? |

| Answer | You may redeem your mutual fund units held in demat form through your DP or Stockbroker. SPEED-e users may submit redemption request online also. |

| 8. | What is the procedure to redeem the mutual fund units held in demat form through my DP? |

| Answer | You need to submit a duly in Redemption Form (RF) to your DP. After necessary checks, your DP will forward your request to concerned AMC / Registrar. After undertaking necessary verifications, redemption amount will be credited to your filled linked bank account directly by AMC / Registrar. You may give redemption request for a specific quantity or all the units or for a desired amount to your DP. |

| 9. | What is the procedure to redeem the mutual fund units held in demat form through stockbroker? |

| Answer | You need to give a redemption order to your stockbroker. In addition, you need to submit Delivery Instruction Slip to your DP to transfer the mutual fund units to the designated CM Pool account of NSE Clearing Limited / Indian Clearing Corporation Limited. |

| 10. | Can I transfer the mutual fund units from one demat account to another demat account? |

| Answer | Yes. You can transfer mutual fund units from your demat account to any other demat account of your choice (held with same or different DP / depository) except for mutual fund units which are under lock-in status for any reason. |

| 1. | When the dividend and shares are are transferred to IEPF Authority?? |

| Answer | All dividends and shares, which remain unpaid or unclaimed for seven consecutive years due to any reason, are transferred by respective companies to Investor Education and Protection Fund (IEPF) Authority. IEPF Authority is a statutory body, constituted under the provisions of Companies Act, 2013. |

| 2. | What is the procedure for claiming the dividend and shares that have been transferred to IEPF Authority? |

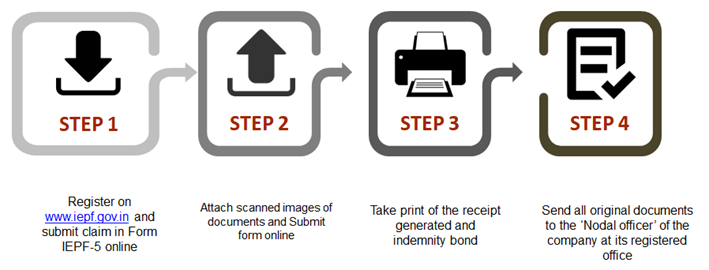

| Answer |

Investor or his / her authorized representative need to submit claim to IEPF Authority to receive unpaid dividend and/or unclaimed shares. After verification of the claim, company confirms the claim to IEPF Authority. The IEPF Authority then initiates refund to claimant in his / her Aadhaar linked bank account through electronic transfer. In case the claim is for shares, they are credited to demat account specified in the claim form. The complete process and documents required are shown in the diagram below. One applicant can file one claim form for each company in one financial year. For more information, please visit http://www.iepf.gov.in/. It is important to know that all companies need to publish details of unclaimed shares and dividend on their website.

|